مرگ بر آمریکا

سپاه پاسداران انقلاب اسلامی

Not quickly.

Not easily.

Not inexpensively.

It is true, as Trump boasted, that an unusually large number of oil tankers have been booked to load U.S. crude oil since America forcibly seized control of the world's primary oil shipping route.

Despite his ill-informed braggadocio, the US is not equipped to process the scores of VLCC (very large crude carriers) headed toward America. The backlog will take months to clear.

The logistical challenges of loading empty supertankers with oil include increased operational costs due to longer empty voyages and capacity constraints that force the use of smaller vessels or multiple shipments.

Trump's simple-minded supporters with no knowledge of the challenges of transhipping petroleum and LNG (liquid natural gas) clap like seals, anticipating an economic bonanza from Trump's pritatical activities in the Persian Gulf.

They are doomed to disappointment.

Filling a 2 million gallon supertanker, (let alone dozens of them) is not as easy as gassing up a pickup at the local convenience store.

Each VLCC can carry roughly 2 million barrels of oil, so the group represents massive potential export volume (over 120 million barrels from the VLCCs alone).

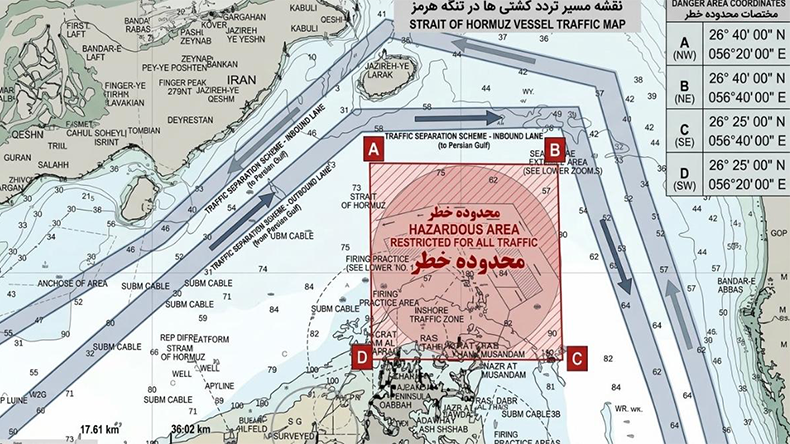

The influx stems from a sharp disruption in Persian Gulf oil flows (exports through the Strait of Hormuz aredown ~92%, from 20 million to just 1.5 million barrels per day due to the American blockade).

Trump and others may view this “swarm” as a huge boon; proof of surging global demand for American oil, an export windfall, and a geopolitical win for U.S. energy dominance.

However, the facts (backed by current EIA export data, port logistics, and global inventory trends) is that it is not the straightforward economic victory it may appear to be.

Here are the main reasons:

1. U.S. export infrastructure cannot handle the volume quickly

- Current U.S. crude export rate (as of January 2026 data cited): ~3.9 million barrels per day.

- Practical maximum capacity: around 4–5 million barrels per day.

- Loading even the 60+ VLCCs alone would require moving ~120 million barrels. At realistic Gulf Coast throughput rates, this creates severe bottlenecks at key terminals (e.g., Houston, Galveston, Louisiana Offshore Oil Port/LOOP).

- Result: Tankers will face long waiting times, congestion, and delays. This is not a simple “turn on the tap” scenario. Ports and loading infrastructure have physical and operational limits that cannot scale instantly.

- The tankers are rushing to the U.S. precisely because Persian Gulf supply has collapsed. Global oil inventories are already drawing down sharply (218 million barrels in recent data, with an even steeper drop projected for 2026).

- U.S. exports cannot ramp up fast enough to replace the lost Middle East barrels. Even major Saudi loading ports like Yanbu are capped at ~4.5 million barrels per day—far short of what the redirected tanker fleet needs.

- Outcome: Worldwide crude shortages → spiking oil prices. Because oil is a global commodity, U.S. consumers will still see higher gasoline, diesel, and heating-fuel costs, offsetting any domestic producer gains.

- Many U.S. refineries are configured to process heavier imported crudes; domestic shale/fracking output is lighter and requires blending or export. The sudden export surge strains this balance.

- The U.S. is already drawing from the Strategic Petroleum Reserve (SPR) to cushion shortages. This depletes emergency stocks rather than building energy security.

- Oil producers and exporters may enjoy higher prices and strong demand in the near term.

- But the video emphasizes the longer-term downsides: global economic ripple effects, higher fuel costs for American households and industries, supply-chain disruptions, and the risk that prolonged Persian Gulf bottlenecks keeps the tanker swarm (and price volatility) going indefinitely.

The U.S. simply lacks the immediate export infrastructure and spare capacity to turn the situation into the rapid, low-pain boom some political rhetoric suggests.

Instead, Trump's boasting obscures the fact that his cowardly bullying risks higher domestic fuel prices, logistical gridlock, and accelerated SPR drawdowns, exactly the opposite of a win.