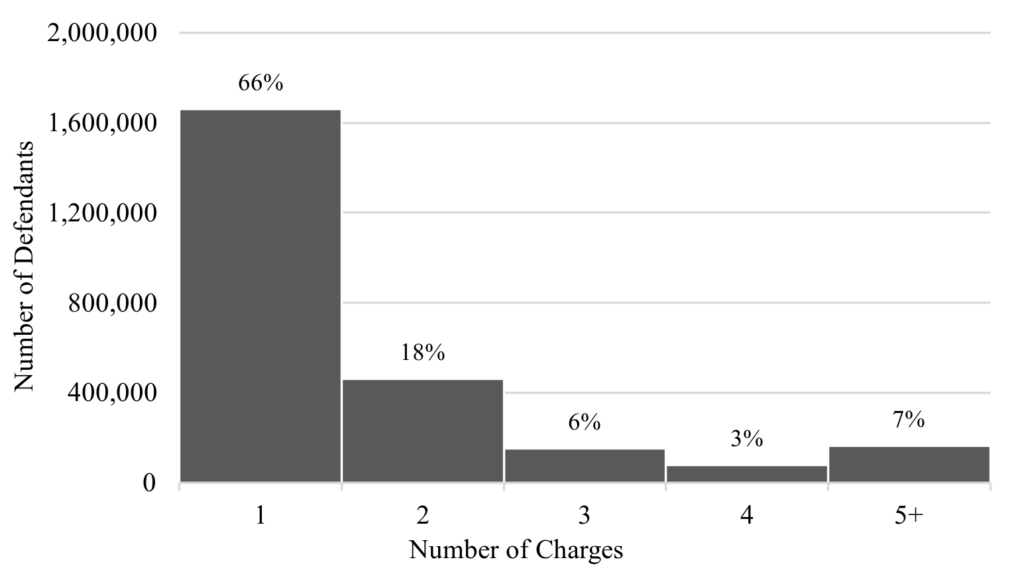

It was a single instance of alleged fraud turned into 34 counts by making each entry, related to the same project, a count. That is, the prosecution alleged that each time Trump made a ledger entry within the same project it was a separate and unique felony. That's complete bullshit and the epitome of charge stacking.

No, the two are different. James sought a civil prosecution for Trump. The charges against James are criminal. The difference is that James alleged Trump exaggerated or otherwise falsified loan documents, but not where these could be criminally charged. She then claimed that those falsifications resulted in a loss. The banks involved said this was bullshit and that they did their due diligence and were not harmed. The judge, who openly despised Trump ruled in James' favor in a bench trial. He and James both knew they couldn't trust a jury to come to a finding of Trump being libel for civil losses in that trial. The NY appeals court is already seriously questioning and doubtful of the findings in that case.

Normally, you have to show that a party was harmed or suffered loss. The banks involved with Trump testified they suffered no loss or harm by Trump's actions.

In James' case, the documents stated right on them that lying or misleading statements could result in criminal, felony charges. It is indisputable that James lied and made misleading statements on the loan documents. Her defense to date is that it didn't matter, that it wasn't her intention to lie, and that the statements were not really inaccurate. Now, a grand jury has found otherwise and is subpoenaing her.

You obviously don't follow this. Trump's charges were CIVIL NOT CRIMINAL in the James case. That is, James was alleging that one or more parties' lost money due to Trump's actions in private civil loans between two parties. This is something the government rarely, if ever, gets involved in simply because it's between two private parties. The government has no direct interest in this, and the judge's finding enriches the government undeservedly.

In James' case the charges are CRIMINAL. The prosecution is alleging that James lied on various government backed loan documents to get better terms knowing that lying on those documents was a chargeable felony. Here, James is alleged to have lied to the government to get better terms on loans. That is something the government does have a direct interest in.

James did not have jurisdiction under NY State law to bring criminal charges against Trump, so suggesting she SHOULD have brought criminal charges but didn't is disingenuous at best.

Further, the entirety of the case stemmed from Trump's fraudulent inflation and deflation of property values in his bids to obtain mortgages. That's mortgage fraud. It's also insurance fraud, tax fraud, wire fraud (since the Fed Reserve would be involved in wire transfers), appraisal fraud (which is really just mortgage fraud in another name), et cet.

I see that the Grand Jury has subpoenaed the 1003, but not James, herself. Do you have a link or some kind of evidence that she's been subpoenaed?

But hey, why keep speculating. How's about we have a look-see?

The 2001 Brooklyn property, and give it a quick review.

- Mortgage from Letitia James to Chase Manhattan Mortgage Corporation dated February 14, 2001 and recorded among the Land Records of the City of New York in Reel 5120, page 2418:

- Has a 1-4 family rider attached to and made part of the mortgage. Pretty bog standard for a residential property.

- The allegation is that the property has FIVE units, not FOUR, and that James lied about the number of units to obtain an FHA-insured mortgage, thus committing mortgage fraud.

- The City of New York Department of Finance shows that the property is assessed with FOUR units.

- ALL FHA mortgages, even back in 2001 when she bought the property, require a physical appraisal which must be reviewed by the lender as a part of the loan application process. That physical appraisal would have needed to show all units in the property.

- If she made changes to the property SUBSEQUENT to the consummation of the mortgage, that would not be actionable for fraud, as at the time the mortgage was made, the property had four units according to the City Assessor and the Appraiser. Unless, of course, the Assessor and Appraiser were ALSO in on the fraud.

- The federal statue of limitations on mortgage fraud being 10 years, this is just plain charge stacking.

My finding based on all publicly available information? No fraud.

The 1983 Mortgage

- Mortgage from Robert James and Letitia James, his wife, to Kadilac Funding, Ltd., dated May 19, 1983 and recorded among the Land Records of the City of New York in Reel 1539, page 1110:

- The allegation is that James and her father signed the documents as husband and wife in order to meet lending requirements and "receive favorable terms".

- This is utter nonsense. A lender cares about the credit worthiness of the parties when lending, they don't care whether or not you're married. They don't care if you're married today, and they didn't in 1983. Whether they were married or not would have ZERO impact on the terms of a loan.

- In almost 30 years in the Real Estate industry, I have seen multiple incidences where a mortgage/deed of trust has an incorrect vesting that nobody caught until it landed in front of me - and I'm sure I missed my share, as well. This is UTTERLY irrelevant to the terms of the loan. It SHOULD be corrected, if it's caught while the loan is still active, but more often than not people will leave it alone, since it really is irrelevant and involves bringing borrowers back to the table to either sign new documents or strike-and-correct the existing, ORIGINAL documents (which often nobody knows where they are any longer).

- THIS is a prime example of charge stacking - especially considering the federal statue of limitations on mortgage fraud is 10 years, and we're looking at 42 years since that $30,300.00 loan was signed.

My findings based on all publicly available information? No fraud.

The 2023 mortgage in Norfolk, VA:

The charge is that James said she would be living in the property as her primary residence in order to get a better rate, and they're basing this on a Power of Attorney.

I DID find a copy of both the mortgage and the PoA, so...

The Power of Attorney states that the property is James' primary residence - this has no affect on the terms of the loan. It could say she lives on Mars, and it wouldn't affect the terms. The Note and Mortgage/Deed of Trust - both based on the 1003 (loan application) and the credit worthiness of the applicants are what matter. This is moot and would not have any impact on the terms of the loan, as the PoA is not part of the note or mortgage but simply an authorization for signing on behalf of the Principal - in this case, James.

In addition, according to James' attorney - and an e-mail sent to the mortgage broker two weeks prior to signing - James notified them that she would not be using the property as her primary residence, but was so-signing as a non-borrower in order to help out her niece. This is so VERY typical - a non-borrowing co-signer not living in the property, but the borrower will be occupying the property. This is not mortgage fraud, it's pretty normal.

I'd have to see the 1003 and note (neither of which are recorded and are not public record) to be sure, but I'm going to go out on a limb and say that the DoJ is engaged in revenge politics and not any actual crime.

We'll see.

FINALLY: You say that the case against Trump doesn't matter because the banks say there was no harm. None of the banks in these matters have declared harm and, what's more, if they had found harm to them by now, they'd have accelerated the mortgages and foreclosed. There are no lis pendens filed in VA or NY indicating any type of foreclosure action - so it looks like the banks don't care, either.

Now tell me why harm doesn't matter for Trump, but does for James.